Insurance is an important practical way of a risk management. It is a protection against the variety of risks and characterized by a willingness to pay to avoid them.

For example: To clarify how risk manager benefits from insurance let's consider the following example. Suppose a person owns a building which costs $ 50,000, as well as other assets in the same worth. There is a 10% probability risk that the building will be destroyed by fire, earthquake, flood or other natural disasters. Thus, there is a 10% probability that the owner will have only $ 50,000 other assets and 90% probability that he will own 100,000 $ (50,000 the building and other assets). Assuming that the owner's usefulness does not depend on other factors, we may say that expected average usefulness is equal to the

E (U) = 0.1U (50000) + 0.9U (100000)

and the expected value is

E(x)=0.1(50000) + 0.9(100000) = 95000

Graphically represented equations

and expected usefulness can be illustrated trough direct line between $ 50,000 and $ 100,000's. The expected usefulness equals to 9 / 10th of the line. According to a risk management theory, the usefulness from expected $95000 is less then usefulness from existing $95000. Moreover, to avoid risks and ensure the usefulness of expected 95000$ risk manager needs to pay a certain (Y) to an insurance company.

If you are offered insurance, then you can pay the premium and the insurance company will reimburse you in a case of loss in a predetermined amount.

Suppose that the premium is equal to the expected loss. In this example, we will receive the expected loss, which equals 0.1 ($ 50,000). It is said that the insurance premium is justified if it is equal to the expected loss. In other words, it is justified to bet on the insurance purchase. The question arises, how much the justified insurance premium must be, for answering the question we will introduce the following simple models that are used in determining the amount of insurance premium.

= income or property without loss

L= the amount of loss

p = the probability of loss

A= compensation in case of loss

If the premium is justified

pA= amount paid for insurance

= ( -L+A-pA) = income in case of loss

=( -pA) = income without loss

If usefulness depends only on income the formula will be

E(U)= pU( ) + (1-p)U( )

To find the optimal amount of compensation we should equalize the derivation of an equation to 0.

= p(1-p) - p(1-p) = 0

Simplifying

=

The derivatives are equal to each other because they calculate the same income with loss or without it. The equation shows that the usefulness and net income should be equal to lose or without.

-L+A-pA = -pA

After solving

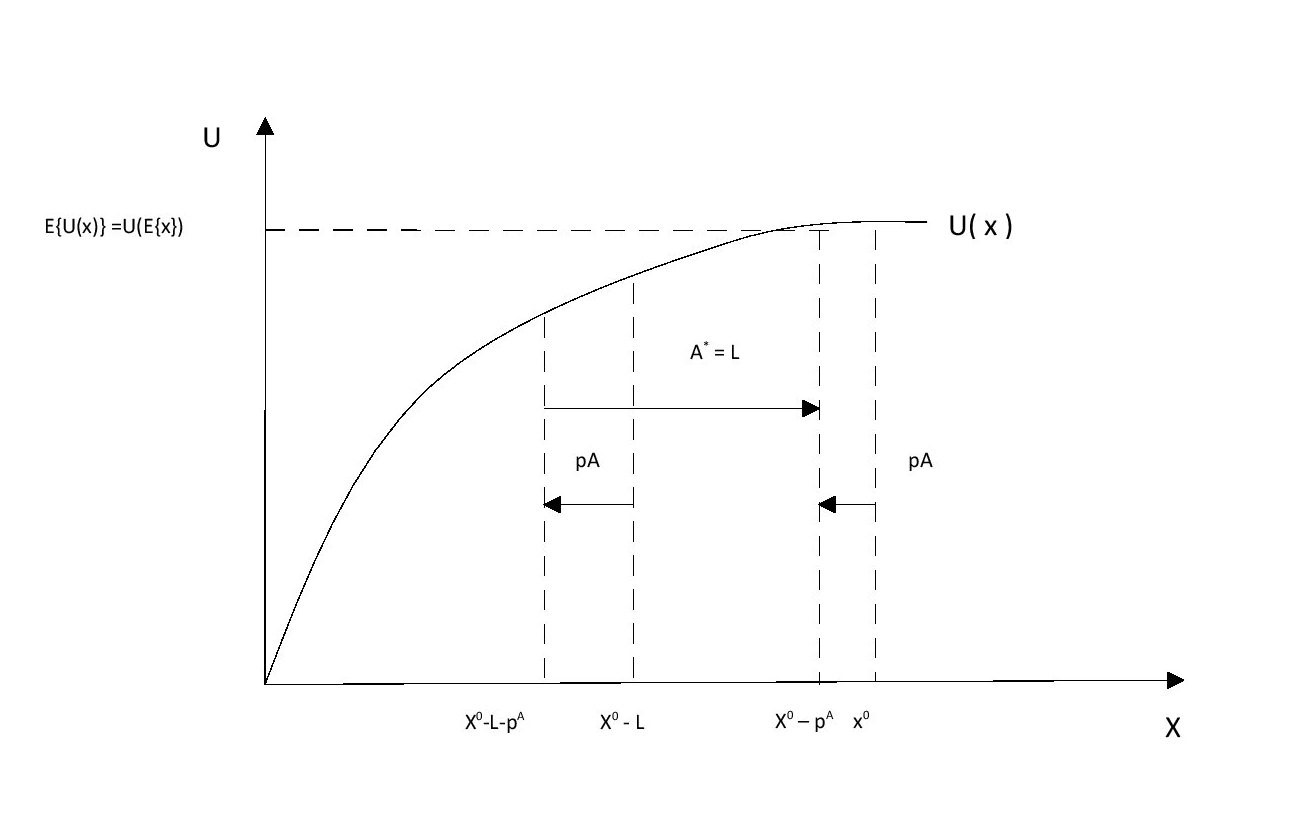

A = L

The equation shows that the consumer is insured in the amount that is equal to the potential loss. As a result, it is clear that consumers will receive the same benefits regardless of loss. The formula

= -A+A-pA= = - pA =

Graphically

In the above example, the consumer pays a $ 5,000 premium from the amount of property (100000$) or from the 50000$ if the loss occurs. But if the loss occurs, the consumer receives a refund in the amount of $ 50,000 consumers receive the same income $ 95,000 whether loss occurs or not.

Insurance and the law of large numbers

Many insurance companies enter into contracts with individuals. Each of these contracts has a corresponding risk of loss. Which means that the compensation has random value, but in one of the rules, which is in widely used in probability theory (the law of large numbers) it is noted that many independent and uniform sales transactions lead to an average value, which is equal to the expected value.

We should mention that the greater the quantity of sample group, the closer will be the result to the expected value. If we do an experiment and toss the coin 100 and 1000 times we will see that in the second case the result will be closer to the expected value than in the first case.

Graphically

The graphic shows that the bigger selection causes the smaller dispersion, which brings to the smaller deviation of expected value. By increasing the number of customers, the particular insurance company also increases the expected risk, but at the same time, it increases insurance payments, which in its term increases at a higher rate than risk.

Futures contracts as insurance

A futures contract is a contractual agreement, generally made on the trading floor of a futures exchange, to buy or sell a particular commodity or financial instrument at a predetermined price in the future. Thus the buyer avoids from hidden dangers related to an uncertainty of prices in the future time period. Assuming that the buyer is risk-averse, we can say that he will buy goods with futures price till the difference between it and expected price will be no bigger than the money for insurance payment

Graphically

In the graph X axis shows us buyer's income after bargain and Y axis shows us utility of that income. The expected average price is and buyer can purchase goods at or prices with a probability of 1/2, where. For one bought a unit of goods at price consumer will have - income and price he/she will have -. The buyer will have income at an average price and will gain E expected utility. The buyer can gain the same utility by buying goods at P futures price because he doesn't need to pay for insurance. In the graph, the difference between expected income and futures income is equal to pay for insurance.

( ) - ( ) = γ => P - = γ

If P is less the futures contract is preferable than insurance.